Construction Outlook: Spring 2026

The outlook for GB construction remains one of decline over the years 2026-2028. Following growth of 1.7% in 2025, we expect construction output to drop by close to 3% in 2026, and 2% in 2027

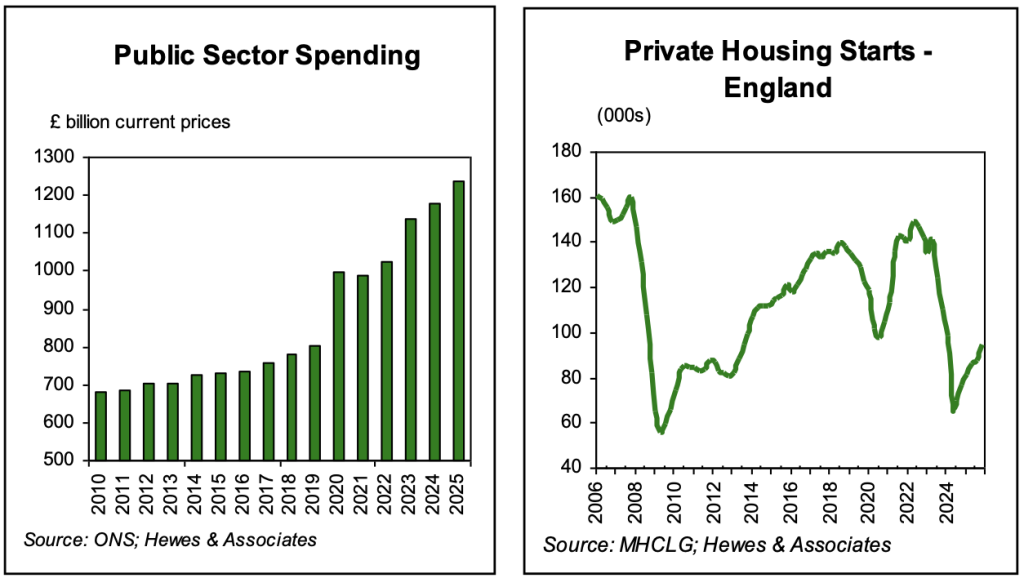

The above outlook relates to a weak economy, political uncertainty, and perhaps most important for construction, a depressed housing market. Over the years 2013-2019 growth in housing new work was crucial to industry growth, with the sector accounting for more around 50% of new work growth. With the end of Help to Buy, and elevated mortgage rates, so the housing market has taken on a much weaker stance, and we do not expect much improvement given economic and political uncertainty.

Alongside current political turmoil, the Government’s 1.5 million housing plan is fast becoming a distant issue. Even so, we have always been of the view that it was more a wish than a plan as it lacked resources and that key ingredient, strong demand for housing. Given current demand and building cost issues, we expect 900,000 houses at most to be supplied across England over the five years 2025-2029.

Works associated with the public sector continue to face a challenging time given extreme fiscal pressures (in the form of a rising public deficit) and weak GDP growth. A key concern of ours is ever growing current spending (NHS and welfare) crowding out capital spending needs. In all, we do not think the Government will be able to reduce the deficit as outlined in the last OBR report.

Infrastructure has a reasonable outlook. Utility works are set to rise over the forecast period, thanks in large part to rising consumer bills. On the other hand, publicly funded works are under pressure: road construction orders are around 50% below the 2022 peak, while investment by Network Rail is relatively depressed (and well below the £7 billion recorded for 2018), and HS2 expenditure is estimated to have peaked.