Construction Outlook: January 2024

The outlook for construction will continue to be affected by lag effects associated with tighter monetary policy and elevated debt levels: in short the UK economy is yet to fully experience the economic impact of near 5% base rates.

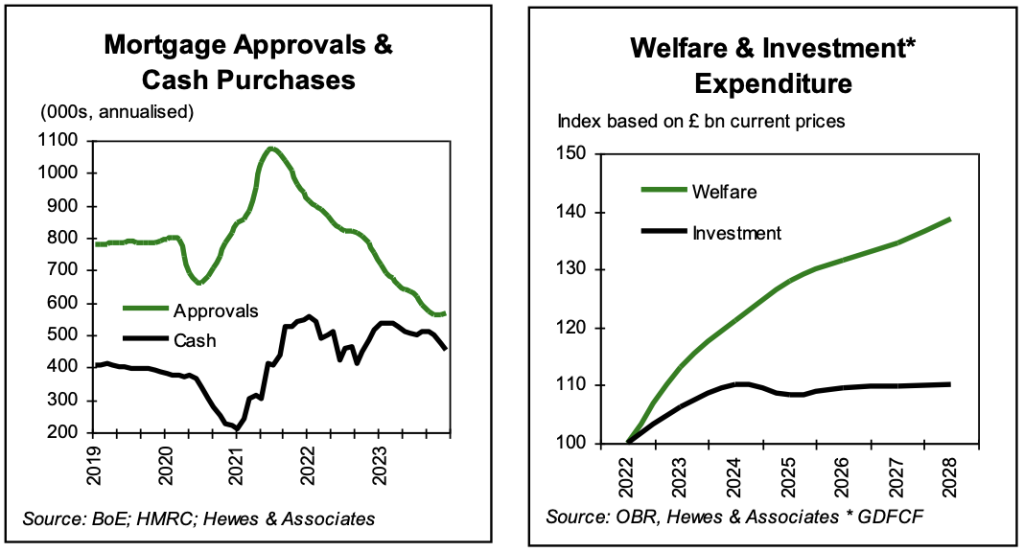

In the public sector raised borrowing costs, alongside elevated debt levels, are serving to limit public policy options, as illustrated by the cancelling of the second leg of HS2. Meanwhile, political priorities mean that for the foreseeable future current spending (on welfare etc.) will take precedence over capital spending, as illustrated below, and so the outlook for public sector capital spending is one of weakness.

In the private sector the trading environment is very different from that seen over the last decade, when businesses and consumers benefitted from extremely loose monetary policy. They now face higher borrowing costs alongside elevated debt levels, and so they too, like the public sector, face restricted economic choices compared with the last decade.

Private construction, in the form of commercial and residential property, clearly faces a very different trading situation as debt is now more costly. While there is much hope that falling inflation will lead to sharp falls in base rates, our assumption is that rates will fall, to around 4% – 4.5% over the short-term. Consequently, housing demand is not forecast to return to recent levels.

As a general election approaches, a change in Government is very likely, and that prompts the question – what will that mean for construction? With the Labour Party talking about fiscal responsibility, and indeed very much subject to the same spending restrictions as the current Government if elected, it is clear that a boost in public investment is unlikely. In the absence of any clear spending promises from the Labour Party, we thus assume a change in Government will have little short-term impact for construction.